The Weekender :The Elephant in the Weekend Room

It’s a good moment to revisit just how far off the reservation Japanese real rates remain compared to the rest of the developed world.

The Circus of Competing Narratives

Markets tiptoed into the weekend like tightrope walkers above a circus of competing narratives—tariffs, tech earnings, and Fed theater. Friday’s session was less a decisive move and more a cautious balancing act, as investors tried to read the tea leaves on inflation, monetary policy, and Trump’s next tariff gambit.

The S&P 500 and Nasdaq opened with some pep in their step, still riding Thursday’s AI sugar high after new record closes. But that early energy fizzled, and the indices ultimately drifted sideways into the close, like traders hesitating at a yellow light. The Nasdaq eked out another all-time high, but the S&P 500 and Dow slipped slightly, unable to maintain their footing as rally fatigue set in, as you can almost feel the market begging for a breather.

The University of Michigan data showed one-year inflation expectations dropping sharply to 4.4% from 5%—a meaningful revision that, in theory, should have ignited a more spirited rally in rate-cut bets. But instead of a surge, the market merely offered a polite nod. At this stage, traders are already riding a tailwind from recent softer inflation prints and know all too well that the U. Mich inflation gauge can sometimes carry political noise.

The result? Tepid reaction. Stock market operators weren’t in the mood to chase doves without a more potent catalyst, more so with earnings season underway. With Big Tech valuations already priced for perfection, investors were more interested in hard upside surprises than soft macro sentiment. In short, a lower inflation read is nice, but it’s not enough to pop the cork when what they really want is a blowout quarter from the tech generals.

Netflix, the first Big Tech player out of the earnings gate, delivered a solid revenue print and a wide profit beat. But traders, like spoiled sommeliers, found the vintage a little flat, as some investors were disappointed by a revenue forecast driven more by a weaker dollar than strong demand for the streamer's content—no extra fizz. The stock sagged as investors questioned the valuation runway. At these heights, tech needs to bring fireworks, not just sparklers.

Meanwhile, American Express painted a rosier picture of the U.S. consumer—especially the upper crust. Its strong results hinted that high-end spending is alive and well, even as tariff anxieties loom. That’s the riddle for equity markets right now: consumers keep swiping, but the backdrop is a foggy cocktail of trade friction, central bank signaling, and geopolitical static.

And that brings us to the Fed’s next act. While Powell himself stayed quiet, all eyes turned to Governor Christopher Waller, a potential heir apparent, who floated a dovish trial balloon on Friday. Waller all but telegraphed his willingness to dissent if the Fed holds rates steady in July, citing a softening private-sector labor market and tame inflation. His tone? Less fire alarm, more preemptive insurance.

“The private sector isn’t as strong as the headlines suggest,” Waller said, pointing to last month’s jobs report where public-sector hiring masked a slackening in private payrolls. Inflation remains subdued, and Waller argued that the modest hit from tariffs isn’t enough to derail the Fed’s ability to ease. It’s a subtle nudge: don’t wait for the engine to sputter—add oil now.

Markets took note. The dollar slipped 0.3%, Treasury yields edged lower, and futures priced in a slight bump in September cut odds—now just above 50%. But even here, there’s no fever. The market remains in a data-watching crouch, eyes on the July 29–30 FOMC meeting, where Powell may or may not play his final guidance card before the succession whispers turn into real bets.

Speaking of succession, Waller’s Friday comments had a not-so-subtle “pick me” energy. While he denied any outreach from President Trump, he didn’t shy away from signaling his willingness to take the chair. But Waller also sent a warning: pick someone the market trusts, or face rising inflation expectations and higher yields. In other words, credibility is currency—debase it, and you pay a premium.

As for Trump, he’s reportedly angling for a minimum 15–20% blanket tariff on EU goods—an escalation that could upend delicate trade talks ahead of the August 1 deadline. It’s another log on the geopolitical fire, one that Wall Street is watching but not yet fearing. The current read: tariffs are background noise, not front-page drama—unless, of course, they start biting into consumer demand.

For now, markets remain suspended in a kind of high-wire hesitation—impressive in its composure, but perilously dependent on soft landings across multiple fronts: the Fed, trade, earnings, and inflation. There’s still altitude left in this climb, but the wind is picking up.

So far, July has played true to form—classic “Bulls of Summer” price action. Despite geopolitical crosswinds and tariff tremors, equity markets have glided higher with the easy grace of a sailboat catching a perfect breeze. The S&P 500 added another 0.6% this week, closing just shy of another record, while leadership rotated between the usual tech juggernauts and defensives like utilities. After April’s momentary panic attack, the index has clawed its way back, now up over 7% year-to-date and 13% from a year ago.

The story beneath the surface? Tariffs are becoming background noise, not a front-row concern. At the onset of the latest tariff drama, the fear was a dual shock: slower growth and stubborn inflation that could corner the Fed into inaction. But neither has materialized in any meaningful way. If the market is now pricing in 10%–15% blanket U.S. tariffs as a “new normal,” it’s doing so with the implicit bet that the cost will be spread out: a bit shaved off producer margins, a little absorbed by importers, and the rest trickling down—eventually—to consumers. But not enough to knock the consumer off balance, and certainly not enough to derail the equity train.

The economic scoreboard this week backed that view. U.S. consumer prices climbed 2.7% y/y in June, up from 2.4% in May, and while core inflation ticked up to 2.9%, the shorter-term annualized trends—2.4% over 3 months and 2.7% over 6—suggest no runaway heat. If you're squinting for tariff fingerprints, the 2.4% jump in core goods inflation was the sharpest monthly move since February, but still within a digestible range.

On the demand side, the U.S. consumer remains a dependable workhorse. Retail sales rose 0.6% in June, a solid 3.5% year-on-year pace. Strip out gas stations, and the trend is even firmer at 4.6% y/y—pointing toward a near-2% real consumption gain for Q2. Confidence is bouncing too, with the University of Michigan sentiment index pulling off its April/May lows, buoyed by buoyant stocks, sticky job strength, and a notable cooldown in inflation expectations.

Put simply, the tariff clouds are out there—but so far, they’ve failed to cast a shadow. Until the data turns or earnings disappoint en masse, this market seems content to stick to its summer rhythm: melt-up over meltdown, resilience over risk-off. It’s July in the markets—and the bulls, once again, are in seasonal bloom.

The Trader View: Riding the Summer Bucking Bull

The week galloped in like a rodeo bull hopped up on espresso and refused to slow down, tossing traders from one asset class to the next in a frenzy of melt-up mania. MegaCap tech roared for the fourth straight week like a turbocharged dragster, while the most-shorted junkyard dogs morphed into greyhounds, clocking their eighth consecutive week of gains and blowing past levels not seen since August 2022. If this is a bear market rally, someone forgot to tell the bears—they’ve been skinned, filleted, and served with a side of AI sauce.

Meanwhile, the Dow sulked in the corner, logging its second red week like a washed-up boxer in the wrong weight class. It’s not just about market cap anymore—it’s about market gravity, and the big money is levitating on narrative helium.

Macroeconomically, the U.S. economy strutted through the chaos like it had secret immunity—CPI and PPI readings were soft enough to lull doves back to sleep, while retail sales and industrial production proved the consumer and manufacturing base still have plenty of fight left. The Philly Fed index pulled off the kind of face-melting turnaround usually reserved for championship comebacks, flipping from -4.0 to +15.9 like a battered team suddenly channeling Michael Jordan in the fourth.

Even the so-called "soft data" stopped being soft—it bulked up, hit the gym, and is now catching up with the hard numbers. If this cycle was a movie, we’ve gone from Recession: The Horror Story to Expansion: The Sequel Nobody Expected.

Crypto was the subplot that stole the spotlight. While Bitcoin tripped over its shoelaces after tapping record highs, Ethereum ran away with the crown, soaring over 20% and busting through $3600 like it had just won regulatory asylum in Washington. After years of being treated like the rebellious teenager of finance, crypto finally seems to have graduated—and Ethereum is now wearing the cap and gown. For the fourth week running, it’s outshining Bitcoin like a Tesla Model S dragging a rusty old Dodge pickup.

In equities, the Mag7 once again made the rest of the S&P look like a chorus line of understudies. Hedge funds? They got taken to the woodshed, with performance plunging to year-to-date lows as short squeezes and momentum surges blew carefully hedged portfolios to smithereens. When the scoreboard reads: “Shorts torched, small caps rally, value over growth, and hedge funds bleeding,” you know you’re not in Kansas anymore—you’re in the heart of a liquidity-fueled fever dream.

Earnings brought more theatrics. Big banks walked into the arena with a cocky swagger after 20–40% pre-earnings rallies, only to find that the bar was set higher than an Olympic pole vault. Half cleared it, half ate mat. Citi emerged the surprise hero, vaulting 8% on the week. Elsewhere, GE and JNJ delivered the goods, while NFLX and UAL slipped on the earnings banana peel.

The bond market had its own Jekyll-and-Hyde act—long-end yields climbed for the third week, steepening the curve like a rollercoaster prepping for its final drop, even as short-end rates eased. Inflation swaps, inexplicably, rose—because apparently, in 2025, even when inflation goes down, inflation fears still get airtime.

The dollar strutted higher for the second week, tossing off rate-cut dreams like a rockstar hurling a guitar into the crowd. Gold held firm, palladium punched to new 13-month highs, and platinum shined its way to levels not seen since 2014. Oil, meanwhile, flamed out, giving up early gains as traders sobered up and remembered that supply and demand still matter.

And just when the market started to feel safe, Trump’s tariff grenade landed with a splat: a proposed 15–20% blanket hit on EU goods. Stocks instantly hit reverse, the rally’s knees buckled, and we were reminded that this tape still trades with one eye on the political fire alarm.

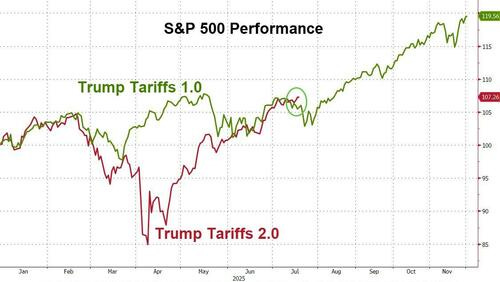

The twist? Trump 2.0 is now outpacing Trump 1.0 in terms of equity market performance. Whether that’s sustainable or a sugar high remains to be seen—but for now, the melt-up machine is firing on all cylinders.

The Elephant in the Weekend Room

Following Friday’s latest inflation print out of Tokyo and with Sunday’s upper house election looming, it’s a good moment to revisit just how far off the reservation Japanese real rates remain compared to the rest of the developed world.

Despite the modest uptick in headline inflation, Japan’s interest rates are still profoundly negative in real terms. While other central banks have been cutting after hiking aggressively or, in the case of the Fed, holding firm, the Bank of Japan remains an outlier through the entire cycle, anchored by yield curve control and a political mandate that has long prioritized stability over preemptive action.

This isn’t just a quirky policy stance—it’s a structural divergence. Even with inflation running north of 2%, the BOJ’s policy rate remains pinned near zero, meaning real rates are still sharply negative. In contrast, the Fed, ECB, and even the Bank of Canada have pushed real rates well into positive territory. Japan, by comparison, is operating on a different axis entirely—closer to financial repression than normalization.

The upcoming election could matter in this context. Should it deliver a fractured result or weaken Prime Minister Ishiba’s leadership, the perceived ability of the government to coordinate with the BOJ—or to push any future normalization agenda—could be further diminished. That’s why USD/JPY remains such a high-beta proxy not just for U.S. yields but for the broader credibility of Japanese macro policy. With real rates still underwater and an election outcome that could inject further uncertainty, the yen’s vulnerability is not just a function of global rates—it’s also about domestic political clarity, or the lack thereof.

This market isn’t climbing a wall of worry—it’s launching itself over it with a jetpack strapped to its back. But just remember: when euphoria becomes consensus and volatility sells at garage-sale prices, the next surprise usually isn’t pleasant.

So keep your helmet on, your stops tight, and your hedges sharp. Because in this circus, the tightrope’s getting thinner—even as the crowd keeps cheering.

Chart of the Week

BofA’s Bull & Bear Indicator ticked up again this week, rising to 6.3 from 6.2—the highest reading since October 2024. It’s inching ever closer to that magic number 8, the contrarian “get out while you still can” line in the sand. The fuel? Torrents of inflows into emerging markets and high-yield credit, paired with falling cash levels among fund managers—a classic cocktail of optimism with a chaser of FOMO.

But here’s the kicker: we’re not at red-alert levels yet. What would push this indicator over the edge? Picture this—more than $25 billion rushing into equities like a stampede at a Black Friday sale, over $3 billion flooding into junk bonds, the S&P 500 screaming past 6400, and hedge funds scrambling to cover their S&P shorts in panic.

In other words, we’re a couple of headlines and a couple of billion away from full-blown melt-up euphoria. And as any seasoned trader knows, once this thing hits an 8, history suggests the fun doesn’t end with a soft fade—it ends with a slap.

Running Update

The good news? I’m making the most of my weekday runs from a training perspective. Keeping things right at LT1—top of zone 2, with a bit of upward drift—I’m clocking endurance scores about 200 points above my yearly average. Still 200 off peak, but hey, progress is progress.

The problem—the one that’s been dogging me all cycle—is stacking up more kilometers in the logbook. Take today: I teed everything up perfectly. Took Friday easy, rested up, the tank was full. But for whatever reason, the legs? Dead weight. Like I was running in molasses. I just can’t seem to win.

Sure, I logged the distance, but it wasn’t that effortless cruise I’d imagined. Running’s got to be the most unpredictable hobby out there. Still, you roll with it, have a laugh, and get ready to lace ‘em up again tomorrow.

FX Alert: Election Jitters Put USD/JPY on the Launchpad

This Sunday’s Upper House elections are casting a long shadow over Japanese markets, with JGBs and the yen both looking uneasy — like poker players holding a weak hand at a high-stakes table.Thanks for reading The Dark Side Of The Boom! Subscribe for free to receive new posts and support my work.

Good morning Steve.

Hope you're doing well!

Glad to read all your financial reports here and elsewhere. You're the best source of valid information on the FX and oil markets.

A BIG THANKS for your incessant will to keep us informed. Yesterday you wrote five (5) reports.

I'm doing well and sending you my best regards.