Martinis, Multiples, and Melt-Ups: Welcome to the 6,300 Club

At the heart of this revelry? A potent blend of strong corporate earnings and economic data that keeps putting theory-heavy recessionistas on mute

Afterparty on Wall Street’s Rooftop

The S&P 500 just served up a top-shelf rally cocktail—part earnings daiquiri, part consumer data martini, both shaken with a twist of “Goldilocks” swagger. Thursday’s session wasn’t just another green day; it was a full-blown afterparty on Wall Street’s rooftop. The benchmark index closed at a record 6,297.36, its ninth new high of the year, while the Nasdaq danced into double digits, notching its tenth record close of 2025. Even the Dow—usually the dad at the disco—joined the groove, tacking on over 229 points.

At the heart of this revelry? A potent blend of strong corporate earnings and economic data that keeps putting theory-heavy recessionistas on mute. PepsiCo popped 7% after crushing expectations like a Pringle can, and United Airlines soared 3% on stronger-than-expected earnings. In fact, of the 50 S&P companies that have reported so far, 88% beat the Street. That’s not a beat rate—it’s a victory lap.

And then came the data, dressed to impress. Initial jobless claims dipped to 221,000. Retail sales rebounded 0.6% in June, flipping the script from May’s -0.9% clunker. Even more important for the GDP geeks: the Control Group—retail’s direct pipeline into growth metrics—rose 0.5%, pushing the YoY figure to a solid 4.0%.

You can practically hear economists recalibrating their models with gritted teeth. For all the hand-wringing from ‘soft’ survey data—the confidence polls, the business outlooks—the hard numbers are telling a very different story. The American consumer, allegedly fatigued and fretting over inflation, is out there swiping cards like it’s Black Friday on repeat.

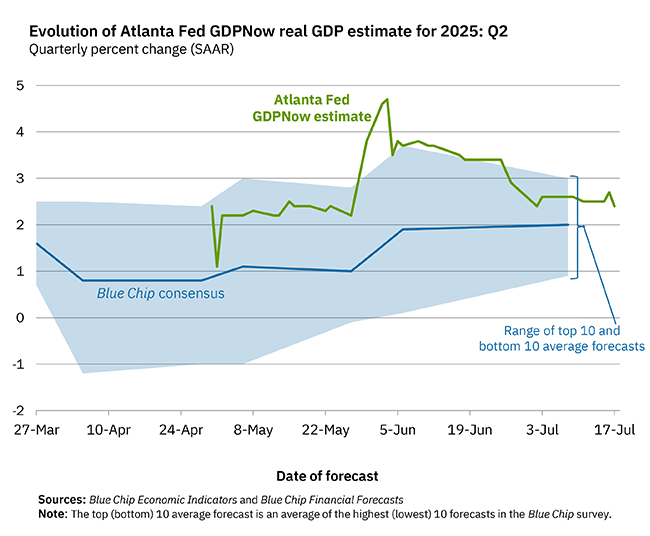

The Atlanta Fed’s GDPNow model now points to 2.4% growth in Q2, comfortably above consensus.

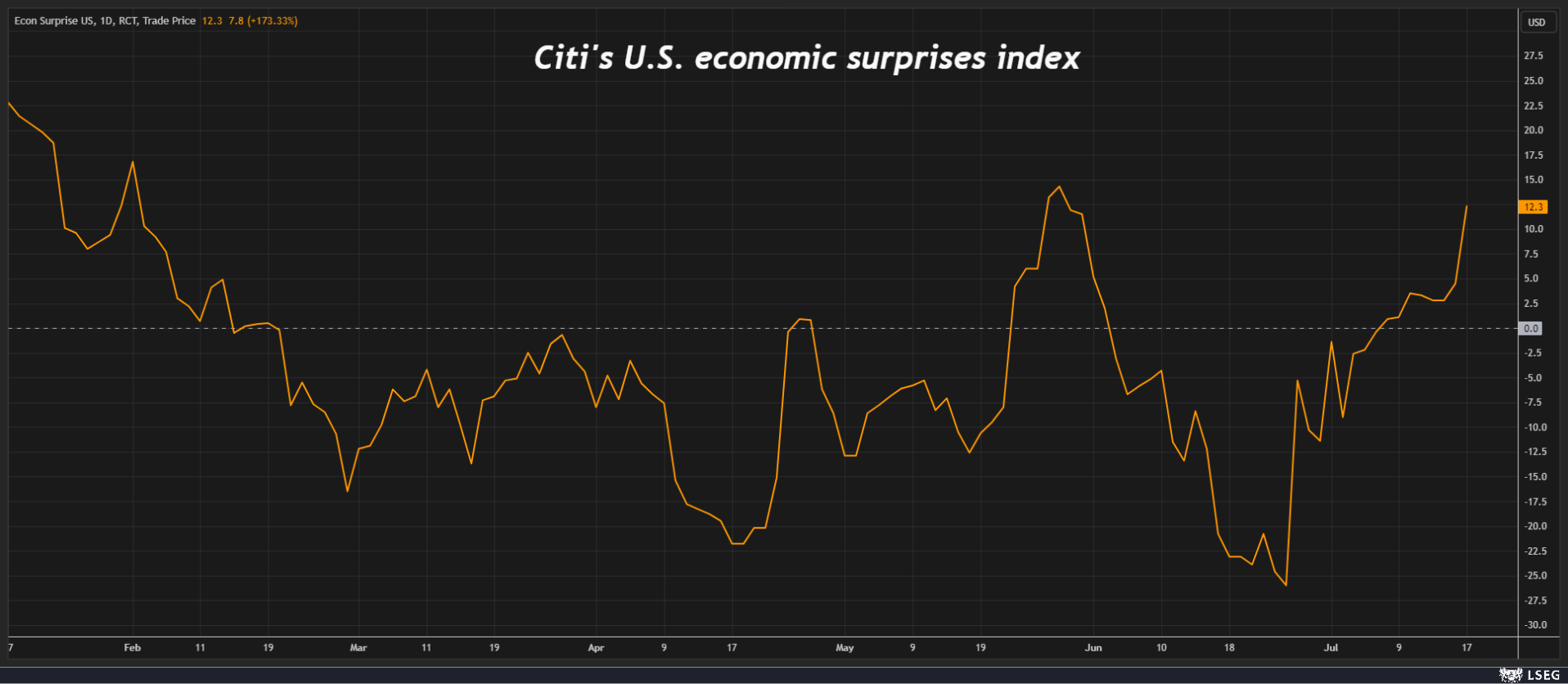

Citi’s Economic Surprise Index has broken out to a two-month high. It’s as if expectations were left in a post–Liberation Day hangover while the real economy got back to work.

Amid the chaos of Powell firing rumours and tariff brinkmanship, the market tuned out the political white noise and tuned into fundamentals. In fact, Wall Street’s ability to brush off political theatre and focus on earnings and data feels almost...mature. Don’t worry—it won’t last.

Still, with earnings season just getting started, and early reports reassuring rather than revolting, the market’s high valuation suddenly doesn’t look so unjustified. If CEOs keep singing the same “resilient consumer” chorus, this rally might just keep climbing the wall of worry—with sunglasses on and a cocktail in hand.

Over in chip land, TSMC’s blockbuster earnings—fueled by AI demand—lifted not just the stock, but global sentiment. The U.S.-listed shares jumped over 4%, pulling semis and tech bulls along for the ride. TSMC remains the blacksmith in the AI arms race, hammering out silicon gold while the rest of the market looks for shovels.

In FX, the dollar found its legs again, partly due to delayed Fed cut expectations (October now looks more likely than September, although I think December is still the more likely scenario). The yen, in particular, is in the hot seat. With Japan’s Upper House elections looming and fiscal risks mounting, the yen slipped to a three-month low. Yields on long-dated JGBs soared, and traders are already eyeing another test of 150 per dollar if Sunday’s result shakes confidence further.

Meanwhile, bond markets continue to feel the heat. Long-end yields across the U.S. and Europe are being pulled higher by Japan’s contagion risk.This is one of those quiet crosswinds that can morph into a gale if left unchecked.

Trade, too, refuses to be ignored. Trump’s latest mood music hints at an imminent deal with India and a “possible” one with Europe. Meanwhile, Commerce Secretary Lutnick is burning up the diplomatic phone lines with Japan, and Treasury Secretary Bessent will be in Tokyo Friday. There’s no formal handshake yet, but markets are sniffing for signals.

All told, the market’s mood has shifted from wary optimism to borderline exuberance—but not without cause. Earnings are holding up. Data is bending stronger. And despite the political drama, the tape suggests that the real economy still has some legs.

As ever, don’t get too comfortable—this market still moves like a jazz solo: confident, but ready to improvise on a dime.

The Trader View: Markets Go Full Goldilocks, Hedge Funds Go Full Roadkill

If yesterday was Powell-versus-Trump kabuki, today was pure macro pageantry—an immaculate set of prints that had "Goldilocks" written in glitter across the tape. Growth surged, inflation fell, and traders were left wondering whether they’d just stumbled into a central bank fairy tale.

Retail sales blew past expectations like a shopper on Black Friday—up and running, no sign of fatigue. At the same time, import prices came in lighter than an oat milk latte, delivering exactly what risk bulls crave: strong demand with cooling inflation. Toss in a frothy helping of upbeat regional Fed surveys and the narrative practically wrote itself—soft landings, soft prices, and soft shorts getting torched.

But while the economic data whispered “rate cuts,” the market had other plans. The odds for two Fed cuts in 2025 crumpled faster than a hawkish op-ed under a dovish rewrite, yet equities went on a tear anyway. The whole board lit up, with Small Caps leading the charge like they just got off a macro leash. The most-shorted names ripped to their highest levels since August 2022, triggering a squeeze that felt like someone lit a fire under the quant desks.

Goldman’s hedge fund performance proxy? Flattened. Clubbed. The kind of day where you imagine some PM somewhere staring at a frozen screen, wondering if they’re actually long volatility or just long regret.

Meanwhile, Treasuries barely flinched. The curve nudged higher, but with the elegance of a sleepy swan. Two-years tacked on a modest 2bps, 30s didn’t budge. The long end continues its slow waltz around the 5.00% yield line like it’s waiting for a partner who never arrives.

The dollar found its swagger again, wiping out the Powell/Trump freakout from earlier this week and reminding everyone that political noise is just that—noise—unless it changes the path of policy.

Gold dipped, bounced, and hovered just north of $3,300. It’s dancing with headlines but hasn’t broken rhythm. Oil climbed toward $68, quietly pricing in steady demand and perhaps a geopolitical premium that never fully went away.

In crypto, Bitcoin did the Bitcoin thing—flopped overnight, rallied midday, and ended close to flat near $120k. But the real story was Ethereum. It launched to a new cycle high, juiced by ETF inflows that looked like someone finally found the unlock code. The ETH/BTC ratio is climbing out of the abyss with the determination of a junk-rated bond sniffing investment grade.

Still, just when it all starts to feel a bit too perfect, there’s always the killjoy: The Conference Board’s Leading Index quietly rolled over again. A reminder that even Goldilocks stories have a twist ending.

And let’s be honest—if Powell’s going to make a move without the specter of political interference looming large, he might need Trump to take a golf weekend. Because as it stands, even if the data screams "cut," the optics scream "don’t."

For now though, the market’s wearing its shades, blasting “Happy” on the speakers, and pretending that fairy tales do come true—at least until the next CPI ruins the mood.

Trump Has Yet To Cross the Rubicon

While some corners of the mainstream U.S. business media are already drafting obituaries for Fed independence, breathlessly insisting that Trump has crossed the Rubicon with Powell, traders aren’t buying it. Whether the Fed Chair is shown the door next week, nudged toward resignation in six months, or limps to the finish line next May, markets aren’t treating this as a constitutional crisis—they’re treating it as theatre.

And that’s the real twist: what’s almost more astonishing than Trump’s barrage against Powell is how unfazed markets remain. Decades of orthodoxy held that even the hint of political meddling in monetary policy would send risk assets into a tailspin. But this market has evolved an almost Teflon-coated exoskeleton. It doesn’t flinch at jawboning or tweetstorms. It sniffs out bluff from policy shift in record time and prices accordingly.

Equity investors, in particular, seem to have tuned out the noise. They've seen this show before: the lead actor roars, the headlines spiral, and then... nothing. As long as earnings hold up and the economic data hums along, Wall Street’s not tossing out its playbook just because Trump threatens to rearrange the Eccles seating chart.

While some corners of the mainstream U.S. business media are already drafting obituaries for Fed independence, breathlessly insisting that Trump has crossed the Rubicon with Powell, traders aren’t buying it. Whether the Fed Chair is shown the door next week, nudged toward resignation in six months, or simply limps to the finish line next May, markets aren’t treating this as a constitutional crisis—they’re treating it as theatre.

And that’s the real twist: what’s almost more astonishing than Trump’s barrage against Powell is how unfazed markets remain. Decades of orthodoxy held that even the hint of political meddling in monetary policy would send risk assets into a tailspin. But this market has evolved an almost Teflon-coated exoskeleton. It doesn’t flinch at jawboning or tweetstorms. It sniffs out bluff from policy shift in record time and prices accordingly.

Equity investors, in particular, seem to have tuned out the noise. They've seen this show before: the lead actor roars, the headlines spiral, and then... nothing. As long as earnings hold up and the economic data hums along, Wall Street’s not tossing out its playbook just because Trump threatens to rearrange the Eccles seating chart.

Polymarket Relevance

While I was early to catch the Polymarket wave during the U.S. election—part of that first, quiet cohort of traders mining predictive crowdsourcing markets for edge—it’s no longer just a back-alley signal shop for the crypto-native crowd. The scent has made its way to the marble halls of Wall Street. First, Goldman started paying attention. Now, even Deutsche Bank’s desks are reportedly tuning in.

What started as a fringe curiosity is morphing into a legit alternative data stream. Traders have always chased signal—odds, whispers, flows—and Polymarket offers all three, distilled into real-time pricing on political risk, macro shocks, and event volatility. For big banks already struggling to wring the edge out of consensus forecasts and stale models, this kind of crowd-implied probability is becoming increasingly hard to ignore.

It’s not about taking the market’s odds at face value—it’s about knowing where sentiment is tilting before the street catches on. That edge matters, especially in an environment where the policy path is murky and geopolitical risk trades like gamma.

And make no mistake: if Deutsche’s sniffing around now, that means the rest of the Street won’t be far behind. Polymarket has gone from a crypto-native sideshow to institutional curiosity—possibly on its way to becoming a terminal tab (right beside Bloomberg) in the not-too-distant future.

I'm not sure about drawing trends out of today's action. i think marketeers are so befuzzled

by trumpian extremes, asserted, withdrawn, maybe reasserted, that they are ignoring the future

more than ordinarily. but when it comes to wanting low rates and over-indulging in debt,

trump has done it his entire life and he is predictable in this one matter, so i think the market

should be taking the risk of a trump run fed more seriously. Companys are still selling

front run cheap inventory to make current earnings estimates and consumers (like me) have been buying the front run goods now, and so will be buying less later. Also, a lot of the earnings reports are lower current quarter versus year ago quarter. they are beating lowered expectations

which doesn't mean that much. And there are situations like the one you recently described with Toyota where they are taking some hit to margins temporarily, but are saying that the hit is going

to be too much to bear, so they will have to pass the inflated price thru. the same thing can happen on the importer side, so the pass thru is delayed, but a bigger hit to the consumer as we go forward. why would we need or want interest rate cuts if the economy is so glorioso?

because it isn't really. Commercial real estate losses have been pushed forward and not marked to market, a giant hole in the balance sheets of most banks. even with falling prices on new homes, the housing market is still struggling. so there's a good reason to lower rates.

but trump will want immoderate rapid cuts immediately and when there comes a time when

we need restraint he will not be restrained. these changes in the tax bill impact immigrant consumption, student borrowers consumption, and poor people using snap cards to buy groceries. and the stressed balance sheets of those who lose medicaid...so there's a fair chance that the consumption we are seeing now won't be the pattern for the future.

as wth inflation during the pandemic panic, it's changes to the balance sheet of those who are not ultra wealthy that become widely systemic and whether its inflation, or stagflation, or recession coming up, we are committed to tipping that wider balance. lost federal jobs and

lost jobs in health care research, and the education system as well, fed by parts of the government being disbanded =a lot of people with disrupted incomes...